Build-A-Bear Workshop v1.0: Q2 '23 ER

$BBW: 1-Up Mushroom surprise going into '23 Q2 earnings

Q2 2023 ER on 8/24 (Premarket)

This post focuses on what to expect in Build-A-Bear Workshop’s Q2 ’23 earnings results. I'm going to assume that a savvy reader would've already read through the 2023 10-K before diving into the 'make-your-own' teddy bear cash-flow machine.1 The market is heading into 2Q ER with an EPS consensus of $0.41 and revenue of $101.89M.

It’s my belief that the EPS consensus by the meager two analysts is underestimating the tailwind on BBW’s license relationships with the summer’s blockbuster IPs. The Super Mario Bros. Movie was released on April 5th, grossing over $1.358B worldwide and setting multiple box-office records. Let's also not forget the successes of Marvel’s Guardians of the Galaxy Vol. 3 (5/5/23) and Across the Spider-Verse (6/2/23). The results for the period cover from May 1st to July 29th.

Jakks Pacific’s Q2 ER results as a preview to $BBW’s ‘23 Q2

A decent comp for the summer blockbuster tailwind thesis is its brother in the IP toy business, Jakks Pacific ($JAKK). Without delving deep into Jakks’ finances, it has similar fundamental metrics to BBW; it is also a classic value company, trading at 2.18x P/E, while $BBW is at 7.94x P/E. More importantly, these two share nearly a zero debt-to-equity ratio. Unfortunately, being “value” is not what moves these consumer discretionary names at the moment.

$JAKK recently highlighted the most talked about film releases in their recent earnings call on July 27th:

“The Super Mario Bros. Movie…is driving demand for both our classic evergreen Nintendo product line as well as the new product range inspired by the film…Separately, the Disney, Little Mermaid film has generated over $0.5 billion at the global box office. We've seen great reaction to our Ariel dress, our under the sea exploring Ariel feature doll with lights and music, and our singing seashell necklace that are all inspired by the film. And our Evergreen Disney Princess business is also benefiting, outperforming last year in terms of sell-through at the top 3 U.S. accounts.”

JAKK’s CEO noted that their earnings were propelled by IPs derived from summer blockbusters. In my opinion, this is where the kicker is: JAKK went into its ER with a consensus EPS of $0.51, but ended up with an actual EPS of $1.26, a whopping surprise percentage of 147%!

JAKK’s revenue was slightly below expectations, and YoY net sales for its Toys/Consumer segment decreased by 20.8%. It rallied regardless for a few days, surging by over 15% following its results and retiring long-term debt.

BBW’s co-brands with leading licenses

BBW also holds many of the aforementioned JAKK’s IP licenses, and it’s quite plausible that similar consumer spending habits are reflected in BBW’s Q2 as well.

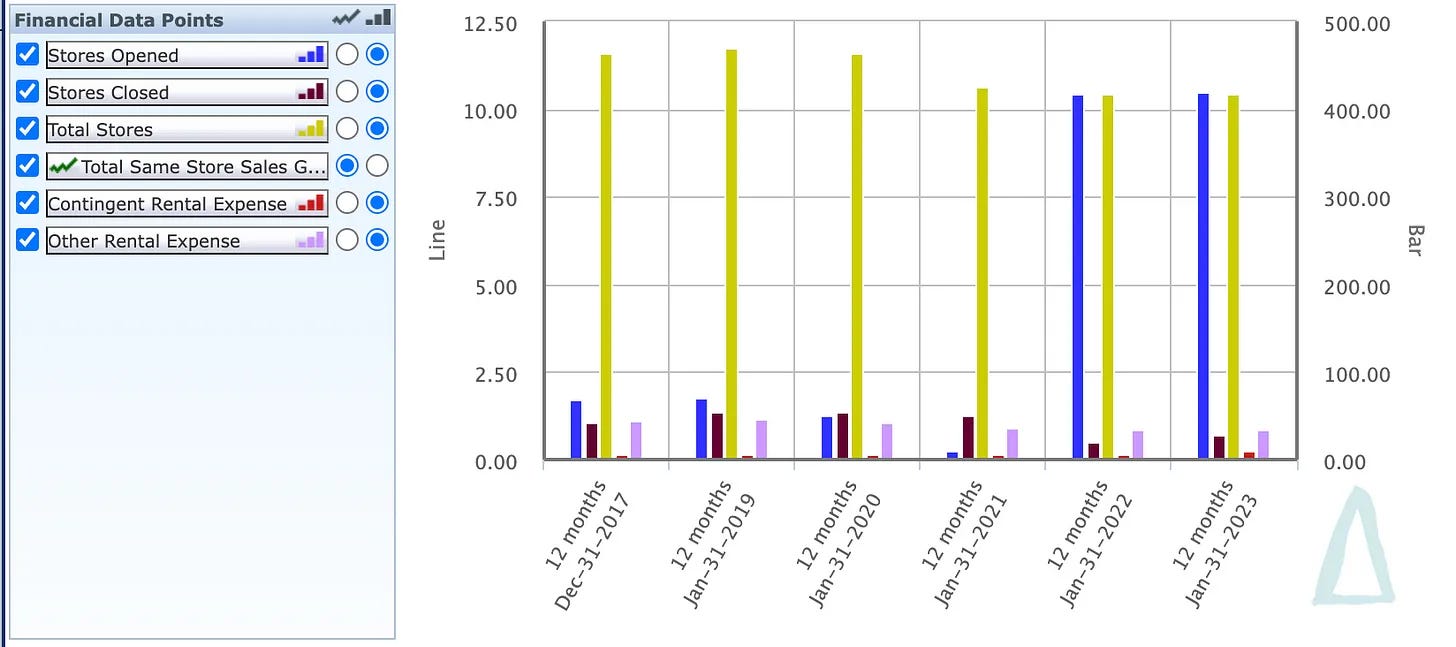

Nevertheless, BBW derives its sales from a broader omnichannel strategy than JAKK. For instance, BBW's branding power and sales are within their own physical retail stores, enabling customers to bring their Frankenstein creations to life. The following store open/closure data shows that the management has been running a tight ship, maintaining a consistent number of stores over the past three years:

BBW Investor Day’s Q2 ER Crumbs

CEO John reiterated BBW’s guidance at the Investor Presentation on June 15th as follows:

Still feel very confident about the 5% to 7% on the top line growth and a 10% to 15% pretax expansion.

I believe the management’s confidence in meeting the guidance stems from BBW’s ability to gather tremendous amounts of first-party data through their loyalty memberships. CEO John noted:

And in fact, our loyalty membership has about an 85%, 86% capture rates when they come into our stores. And those stores generate over 15 million people crossing that lease line every single year.

Another thing to be cognizant of is that BBW’s Q2 revenue expectation has not yet priced in the record-breaking Q1 ’23 results, which delivered the highest revenue, pretax income, and EBITDA in BBW’s history.

Generally, when a consumer discretionary company showcases such a strong quarter, it has a tendency to bleed over to the following earnings. I believe the top and bottom-line estimates going into Q2 earnings are being lowballed, a common phenomenon when there is a lack of broad sell-side coverage. Less coverage is a blessing.

The short-term BBW ER trade in the “asymmetrical disconnect”

Besides the short-term tailwind from summer blockbusters and the sell-side's underestimation of earnings for Q2, another reason to go long is that BBW's fiscal year 2023 has 53 weeks compared to 52 weeks in 2022. For reference, the additional week in fiscal 2023, which will be reflected in the 4th quarter, is estimated to be $7 million in total revenues with approximately 35% flowing through to EBITDA.2 This one keeps on getting better for the year end.

I’ll update on BBW’s charts shortly.

Disclaimer: I have a long position in BBW, January 19, 2024 out-of-the-money LEAPS to capitalize on the potential surprise.

https://ir.buildabear.com/node/19196/html

https://ir.buildabear.com/static-files/763385f6-7fc6-4897-b608-43c573919edd

Great coverage and great writing! Thank you, appreciate it!