Momentum builds for Ralph Lauren

$RL Long entry is might be around the corner soon

It’s been a whirlwind in DC over the past week, navigating the new administration’s hastily issued executive orders. The chaos is part of Miller’s strategy to flood the news cycle and markets with confusion. What’s interesting is the market’s complacency in response to the White House’s tariff news on Canada and Mexico, as well as Trump’s Gaza comment—suggesting it’s merely the “boy who cried wolf” for the fourth time. I expect more bluster headlines and a muted market reaction.

Amid this politically charged week, I’ve kept my eyes on Ralph Lauren.

$RL: Ralph Lauren’s holiday results well above expectations

I had written about my experience visiting a Polo store in New York over the holidays, where the store had low inventory on certain items featuring Americana insignia. Going over the 3Q results, I was not surprised that it did as well as it did. Music to my ears:

Third Quarter Revenue Increased 11%, Ahead of Expectations, with Better Than Expected Holiday Performance in All Geographies Driving Outperformance

Global Direct-to-Consumer Comparable Store Sales Grew 12%, Driven by Positive Retail Comps Across Regions and Channels; Global Wholesale Sales Increased High-Single Digits Including a Return to Growth in North America Wholesale

Adjusted Gross and Operating Margin Expansion Exceeded Our Outlook, with Strong Full-Price Demand and Expense Discipline More than Offsetting Investments in Marketing and Key Cities

Maintained Healthy Balance Sheet with Accelerated Free Cash Flows and Well-Positioned Inventories at Quarter-End

Returned Approximately $500 Million to Shareholders Through Our Dividend and Repurchase of Class A Common Stock This Fiscal Year-to-Date

Raised Full Year Fiscal 2025 Revenue and Adjusted Operating Margin Expansion Outlook Based on Strong Year-to-Date Performance

The results were not unexpected given its presence in the affordable luxury space, but this DTC segment’s 12% YoY growth should garner some attention. Here’s why I believe it’s critical: Polo products have always been a brick-and-mortar brand; thus, making this seamless transformation indicates that its digital campaigns are effectively reinforcing brand power online.

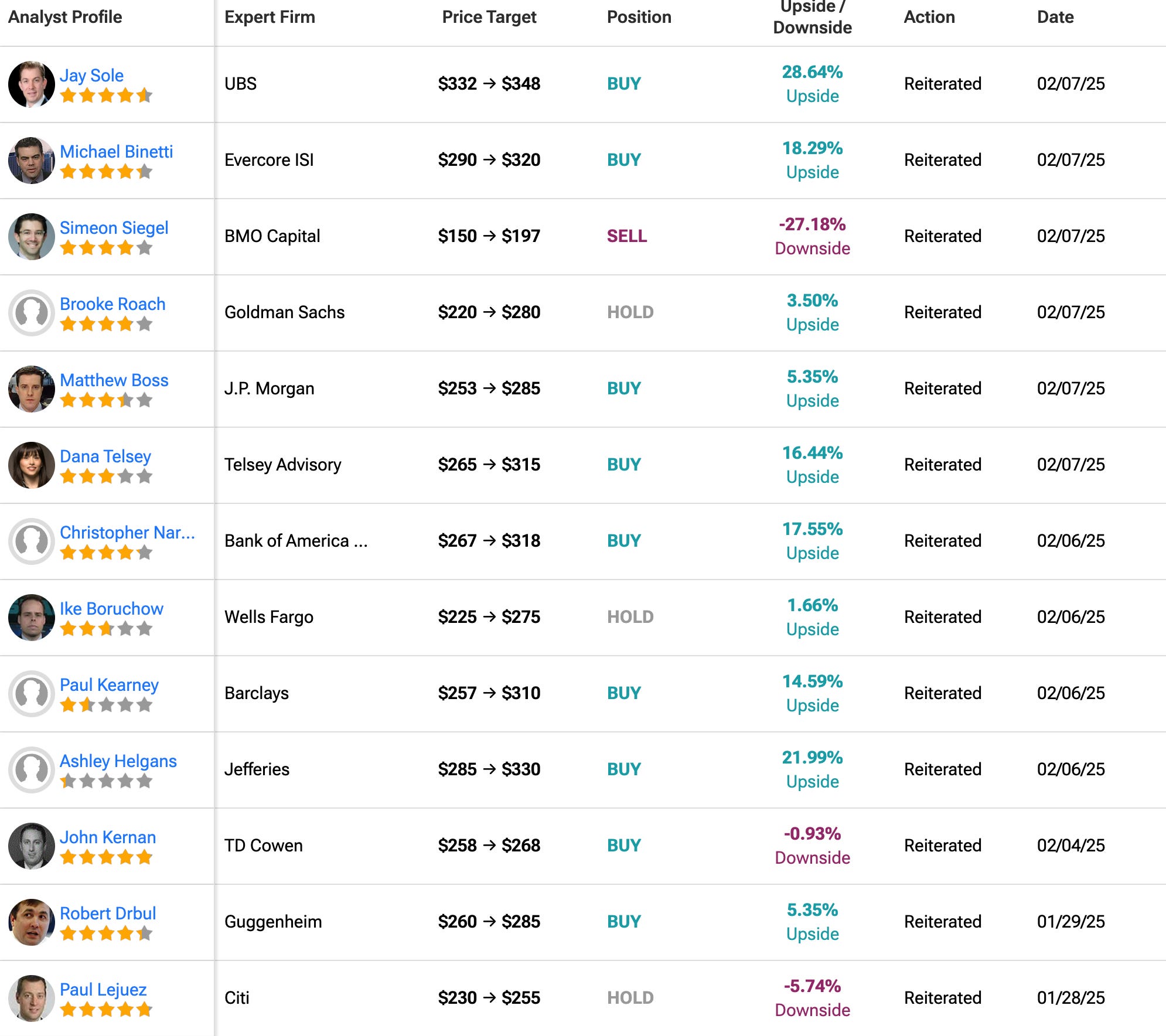

Sell-side adjustments post-Q3 ER

As of February 11, it is trading at $272. The sell-side liked what they saw last holiday season and collectively raised the price target, with a mean of $288.29. In conjunction with sell-side visions, the chart below reflects optimism in its intermediate trend:

It would be a blessing of an opportunity if it can fill the Q3 earnings gap (orange box) for entry in my view.

February is historically the worst-performing month of the year for consumer discretionary, and it’s quite plausible that it reaches that level or drops further to test the 50-day SMA. Ralph Lauren is known for filling gaps and testing key moving averages.

Here’s another look at the chart from a weekly timeframe. When the WMA-10 (purple line) is above the WMA-30 (orange line), it tends to sustain momentum in the intermediate term. If you recall my prior tips on weekly charts, the WMA-10 acts as a magnet, so the stock will typically meet it at some point every few weeks. In this case, my educated guess is that this happens when it fills the Q3 gap.

Capital CIQ Spread on Ralph Lauren

Confirming my prior thesis on holding out to test either the daily MA-50 or the weekly MA-10 before going long, the Capital CIQ Spread supports this view, suggesting that waiting is likely prudent. Here, Ralph Lauren has already reached the CIQ median target of $279.15 and is currently at $272.

A good entry point, based on RL’s historical CIQ spread, is somewhere below 15% from the current CIQ median of $279.15, which puts it at $237. Similarly, this aligns with the SMA-50 at $239.

I’d wait for now but will likely size up for the next trade and set an immediate 8% stop loss upon entry.

I’ll keep you posted and thanks for reading.

-G